Meta Q1 2026 Earnings: US Ad Price +14% and CPC Pressure

Meta reported Q1 2026 results on April 29, 2026. Family of Apps ad revenue hit $55.0B (+33% YoY), ad impressions rose 19%, and average price per ad rose 12% worldwide. The most important line for US advertisers is regional: US/Canada average price per ad increased 14% while impressions increased 13%. Meta does not report CPC directly, but if your CTR did not improve, that price pressure likely shows up in your CPC and CAC.

The numbers

- Total revenue: $56.3B (+33% YoY)

- Family of Apps ad revenue: $55.0B (+33%, +29% constant currency)

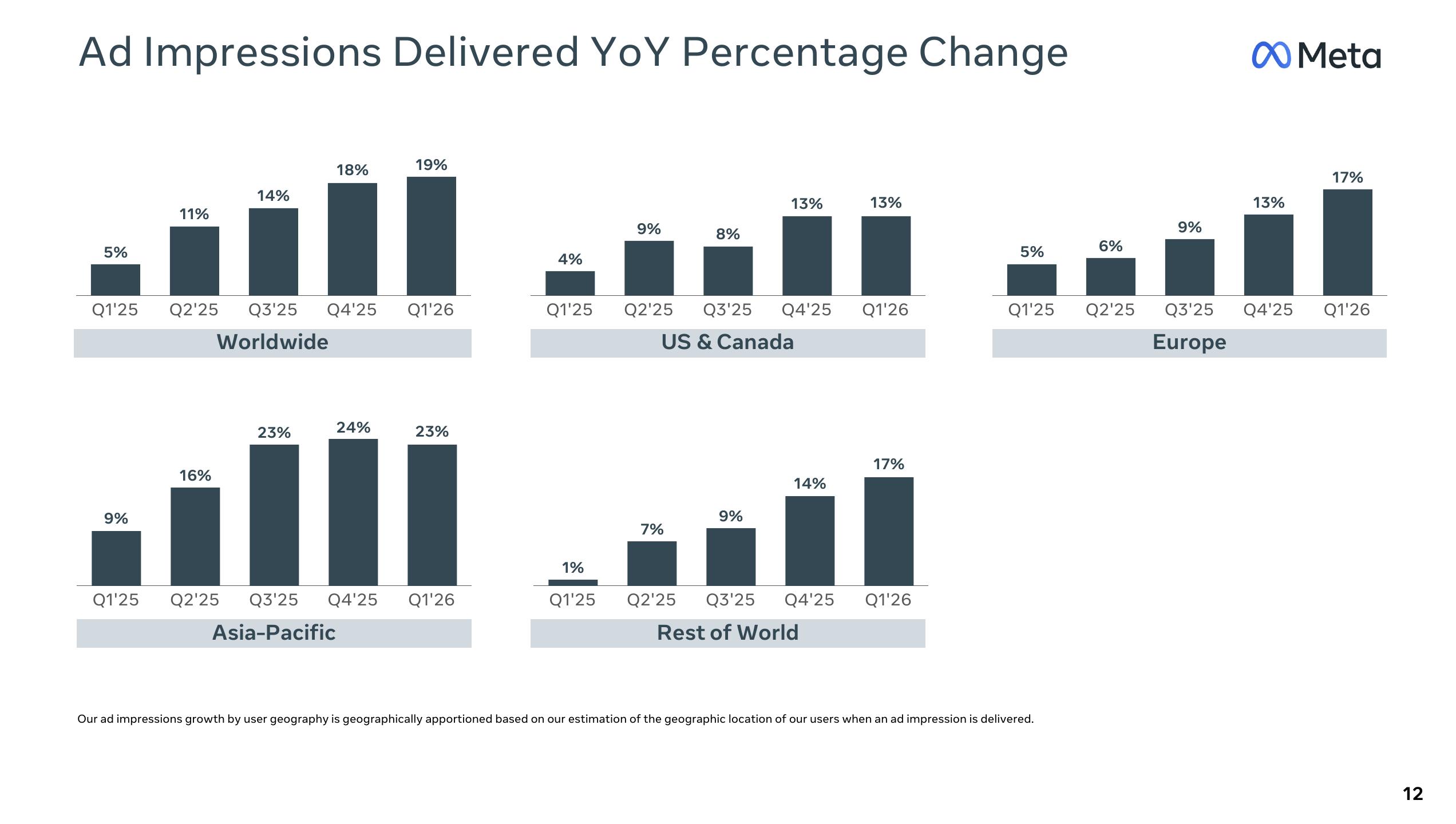

- Ad impressions: +19% YoY (Asia-Pac +23%, Europe +17%, US/Canada +13%)

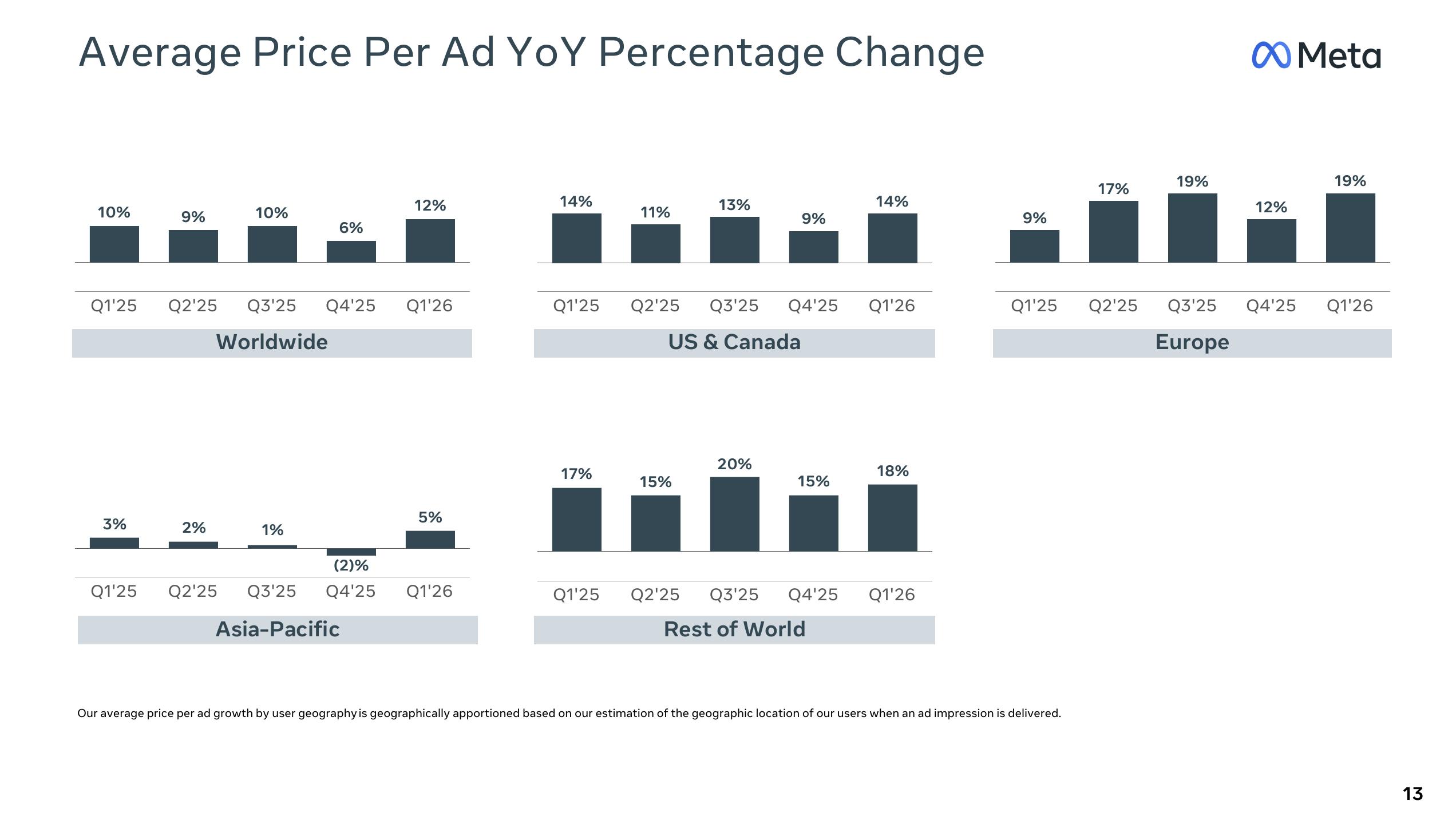

- Average price per ad: +12% YoY (Europe +19%, US/Canada +14%, Asia-Pac +5%)

- Daily Active People (Family): 3.56B (vs. 3.43B Q1 2025)

- ARPP (Family): $15.66 (+27% YoY)

- EPS: $10.44 reported; $7.31 excluding the Q1 tax benefit

- Net income: $26.8B reported; $18.7B excluding the Q1 tax benefit

- Reality Labs op loss: $4.0B

- 2026 capex guidance: $125B–$145B (raised from $115B–$135B)

The US CPC read

The cleanest operator takeaway is not "Meta ads are up 33%." It is that the US/Canada auction got more expensive even as supply kept growing. Meta's regional slide shows US/Canada ad impressions up 13% YoY and average price per ad up 14% YoY in Q1 2026.

That is not the same as CPC. Meta's metric is an average price across delivered ads, while CPC depends on how much you pay for impressions and how often people click. But the math is simple enough for budget planning:

If your effective CPM or auction price rises 14% and CTR is flat, CPC moves in roughly the same direction. A $1.00 click becomes about $1.14 before conversion-rate changes. To hold CPC flat, creative and targeting need to produce about 14% more click efficiency. To hold CAC flat, conversion rate or AOV has to make up the difference.

What advertisers should actually take away

Average price per ad is the budget pressure signal

If you set 2026 budgets against 2025 CPC or CPM assumptions, you're already light. Q1 ad pricing rose 12% YoY worldwide, 14% in US/Canada, and 19% in Europe. The 27% jump in ARPP is the cleanest signal that Meta is monetizing harder per user, not only expanding reach. Rebuild your blended CPM, CPC, and CAC models against Q1 2026 actuals, not Q1 2025.

Asia-Pacific is where impression supply is opening up

+23% impression growth in Asia-Pacific against just +5% price growth means there's genuinely more inventory there at relatively cheaper rates. For brands with APAC expansion on the roadmap, Q2 is a structurally favorable window. Compare that to Europe (+17% impressions but +19% price) where the pricing is now eating most of the volume gain.

$145B capex bet = more aggressive AI-driven targeting

Meta raised the top end of 2026 capex from $135B to $145B, on top of $19.8B already spent in Q1 alone. For advertisers this signals continued investment in ranking, automation, and creative-recommendation infrastructure that surfaces in Ads Manager as more aggressive Advantage+ defaults, more auto-enabled enhancements, and more "auto-injected related media." Expect the silent-auto-on pattern to continue.

DAP +3.8% YoY, ARPP +27% — monetization is the engine

Family DAP grew from 3.43B to 3.56B (+3.8%). The ad revenue acceleration is monetization-driven, not user-driven. That structurally favors Meta's incumbents (large advertisers with existing creative supply) over new entrants who don't have the volume to absorb higher CPMs. Smaller brands need sharper creative testing cadence and tighter geo/time-of-day targeting to compete.

What to check in your account this week

- 1 Pull Q1 2025 vs Q1 2026 CPM, CPC, CTR, and CVR by placement. If CPM is up but CPC is flat, your creative is absorbing the auction pressure. If CPM and CPC are both up, CTR is not keeping pace.

- 2 Separate US/Canada from blended global performance. A worldwide average can hide the US/Canada problem. Meta reported US/Canada price per ad +14% and impressions +13%, which is the zone most likely to pressure US CPC.

- 3 Split prospecting from retargeting. Retargeting can mask auction inflation because intent is higher. Use cold prospecting CPC, outbound CTR, and landing-page-view rate to see whether the auction is getting structurally harder.

- 4 Audit Advantage+ and ad enhancement defaults. Capex investment in AI ranking means Meta will keep auto-enabling features. Document your overrides before you compare Q1 to Q2.

- 5 Check APAC opportunity. If you have APAC-eligible products, Q2 is a structurally favorable window for testing.

Sources

- Meta Investor Relations - Q1 2026 results press release

- Meta Q1 2026 earnings presentation PDF

- Meta Q1 2026 earnings call event page

Don't fly blind on Meta the next time delivery breaks

Meta is shipping more aggressive AI changes through 2026 - capex says so. AdStatus monitors Meta status feeds, plus Google, Microsoft, Pinterest, Amazon, Shopify, ChatGPT, and Claude. Slack alerts within 5 minutes. $10/month.